Does insurance coverage cowl tree falling on automotive? This can be a query that is bought of us scratching their heads, particularly those that’ve had a tree determine to carry out a shock touchdown on their car. It is an actual pickle, a botanical mishap, and a possible insurance coverage headache. We’ll delve into the murky waters of insurance coverage insurance policies, inspecting the specifics of protection for this relatively uncommon kind of harm.

Completely different insurance coverage insurance policies have various clauses, and the specifics of a falling tree incident can considerably influence whether or not your declare will get a thumbs-up or a thumbs-down. Elements just like the age of the tree, the placement, climate circumstances, and even pre-existing tree circumstances can all play a task. Let’s navigate this difficult scenario and discover out in case your insurance coverage firm pays for the tree-mendous harm.

Forms of Insurance coverage Protection

Understanding your auto insurance coverage coverage is essential, particularly when sudden occasions like a falling tree harm your car. Completely different insurance policies provide various ranges of safety, so figuring out what’s lined is vital to avoiding monetary surprises.

Legal responsibility Protection

Legal responsibility protection protects you for those who trigger harm to a different individual’s property or injure them in an accident. It would not cowl harm to your individual car. Consider it because the “different man’s” protection. For instance, if a tree falls in your automotive whilst you’re driving, and it additionally damages one other automotive, legal responsibility protection would seemingly cowl the harm to the opposite car, however not your individual.

The identical applies for those who injure somebody.

Collision Protection

Collision protection pays for harm to your car if it collides with one other object, no matter who’s at fault. This contains impacts with a tree, a parked automotive, or perhaps a stationary object. For example, a falling tree placing your automotive can be lined beneath collision. That is essential as a result of it covers harm even for those who aren’t at fault.

Complete Protection

Complete protection goes past collision, masking harm to your car from perils apart from collisions. This contains harm from falling objects like timber, hail, hearth, vandalism, and even flood. It is basically an all-risk coverage. A falling tree damaging your automotive, even when there isn’t any collision, can be lined beneath complete.

Key Variations: Legal responsibility vs. Property Harm

Legal responsibility protection focuses on the opposite get together’s losses, whereas property harm protection, typically included inside legal responsibility, covers the harm to your individual car. If a tree falls and damages your automotive, legal responsibility will not cowl your damages. Nonetheless, complete or collision protection would.

Protection for Completely different Automobile Sorts

Protection choices may differ relying on the kind of car. For instance, traditional vehicles or collector autos may require specialised complete protection to account for his or her distinctive worth and restoration prices. Luxurious autos could have increased premiums, however the protection quantities might also be adjusted accordingly. This highlights the significance of tailoring your protection to the particular wants of your car.

Insurance coverage Coverage Applicability to Tree-Associated Automotive Harm

| Insurance coverage Sort | Potential Applicability to Tree Harm |

|---|---|

| Legal responsibility | Seemingly covers harm to different autos or accidents to others, however not your individual automotive. |

| Collision | Covers harm to your car if a collision happens, together with a tree falling on it. |

| Complete | Covers harm to your car from any peril apart from a collision, together with falling timber. |

Elements Influencing Protection Selections: Does Insurance coverage Cowl Tree Falling On Automotive

Insurance coverage corporations do not simply have a look at whether or not a tree fell in your automotive; they think about numerous elements to determine if and the way a lot they will cowl. That is essential as a result of they should steadiness defending policyholders with managing their monetary threat. Understanding these elements helps you anticipate the claims course of and probably strengthen your case.Insurance coverage claims for tree-related harm to autos are evaluated based mostly on a spread of things that affect the corporate’s decision-making course of.

These embrace the placement of the incident, the climate circumstances on the time, the situation of the tree itself, and pre-existing circumstances that may have contributed to the harm. The extra info you possibly can present about these elements, the higher your possibilities of a positive final result.

Location of the Incident

Completely different areas current various dangers. City areas, with their denser populations and probably extra regulated tree upkeep, might need a decrease chance of tree-related harm in comparison with rural areas. In rural areas, older timber and fewer frequent inspections may result in increased dangers of falling timber. This implies the insurance coverage firm could assess claims in another way relying on the placement, contemplating the particular environmental context and potential dangers related to the realm.

Climate Situations

Extreme climate occasions, like hurricanes or thunderstorms, considerably influence insurance coverage selections. A tree falling throughout a extreme storm is extra prone to be thought of an act of nature, rising the likelihood of protection. Conversely, a tree falling throughout a light breeze may increase questions on pre-existing tree circumstances, probably resulting in a decreased payout or denial. The severity and period of the climate occasion play a key position within the analysis.

Age and Situation of the Tree

The age and total well being of the tree are essential concerns. A younger, wholesome tree is much less prone to trigger harm than an outdated, diseased, or weakened tree. Insurance coverage corporations could scrutinize the situation of the tree to find out if its deterioration contributed to the incident. Elements equivalent to pest infestation, structural harm, or indicators of decay are all thought of.

A pre-existing situation on the tree, equivalent to a noticeable leaning or seen harm, may influence protection.

Pre-Present Situations

Pre-existing circumstances can dramatically affect a declare. If a tree has proven indicators of weak spot or decay for a substantial time, and this wasn’t addressed or reported, the insurance coverage firm may argue that the harm was preventable. A house owner’s failure to report or handle seen issues, like leaning or cracking, might influence the protection. Equally, if a tree has a historical past of falling branches or has been beforehand marked for removing, this might considerably influence the declare.

Influence on Insurance coverage Claims

| Issue | Potential Influence on Declare |

|---|---|

| Location (rural/city) | Rural areas might need increased tree-related declare frequency, impacting evaluation. City areas could have decrease frequency, however evaluation might be affected by tree upkeep rules. |

| Climate circumstances | Extreme climate will increase the chance of protection, however a scarcity of extreme climate could result in questioning the reason for the harm. |

| Age and situation of the tree | A weakened or outdated tree could end in decreased or denied protection if pre-existing circumstances weren’t addressed. A wholesome tree is extra prone to have protection granted. |

| Pre-existing circumstances | Seen indicators of weak spot, decay, or a historical past of points can result in decreased or denied protection. A scarcity of reporting can considerably influence the declare’s final result. |

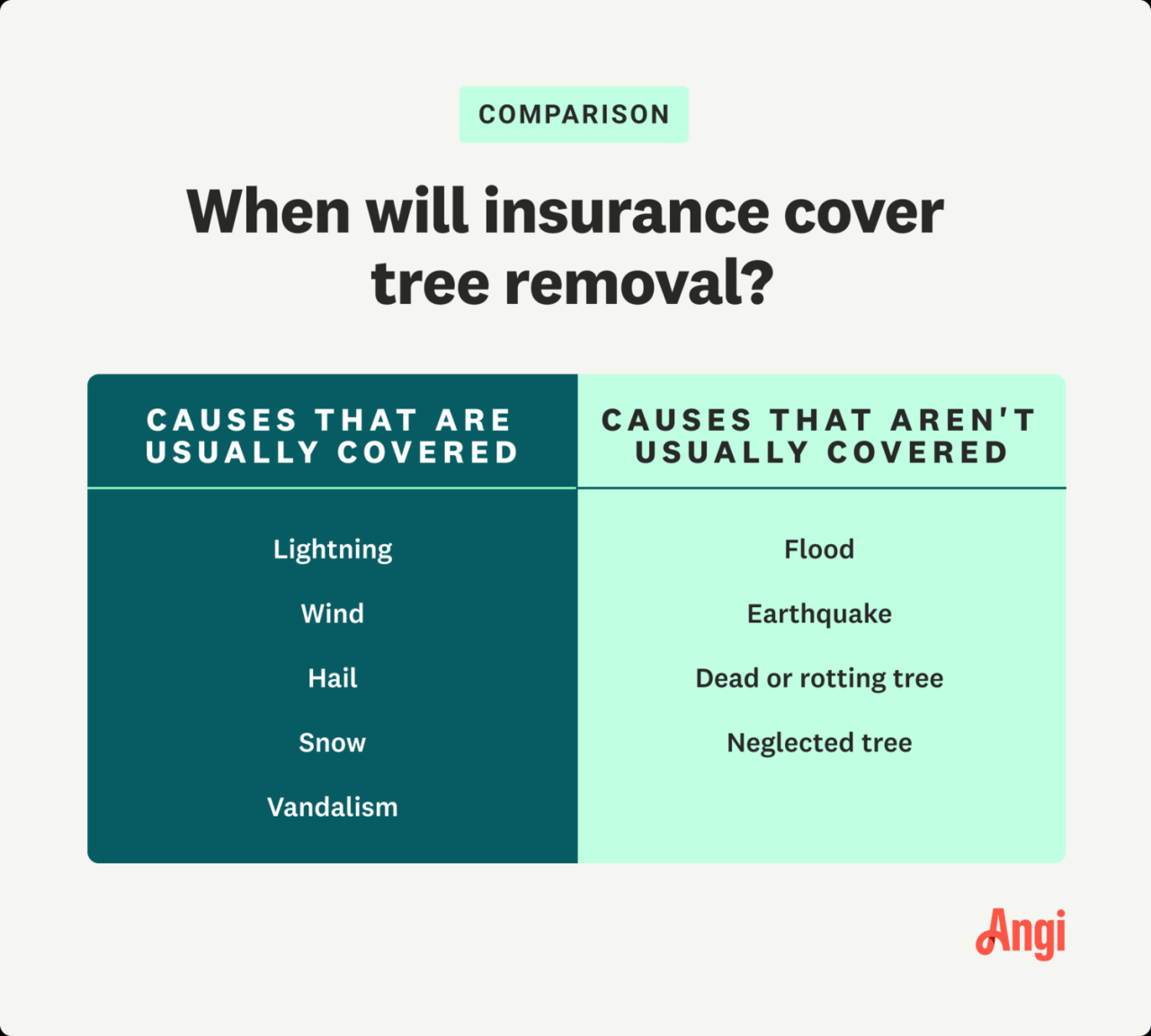

Exclusions and Limitations

Insurance coverage insurance policies aren’t magic bullets; they’ve limitations. Understanding what’s excluded is essential to keep away from disappointment when a tree falls in your automotive. This part dives into frequent exclusions and conditions the place protection is unlikely, serving to you navigate potential pitfalls.

Frequent Exclusions in Auto Insurance coverage Insurance policies

Many automobile insurance coverage insurance policies have clauses that exclude protection for harm attributable to falling timber, significantly if the tree’s situation was a pre-existing difficulty. That is typically as a consequence of complexities in figuring out legal responsibility and the potential for widespread claims. These exclusions are designed to guard insurers from extreme payouts and to handle threat successfully.

- Acts of God/Pure Disasters: Whereas some insurance policies could cowl harm from extreme climate occasions, the protection may not lengthen to a tree falling in your car. The precise wording is significant. If the harm stems from a naturally occurring occasion like a storm, however the pre-existing situation of the tree contributed, the insurer may argue it was a mixture of occasions and never totally a pure catastrophe.

For instance, a coverage may state that “harm from windstorms, hail, and floods is roofed, however not harm from timber falling as a consequence of pre-existing circumstances.”

- Pre-existing Tree Situations: If a tree was recognized to be diseased or unstable earlier than the incident, protection for harm from its fall is likely to be denied. Insurance coverage corporations typically examine the tree’s well being historical past and the potential for the tree’s situation to have brought on the harm. For instance, a coverage may state “harm from falling timber shouldn’t be lined if the tree was recognized to be unsound or diseased previous to the occasion.”

- Negligence of Property Proprietor: If the tree fell from a property you do not personal, and the proprietor was negligent in sustaining the tree, protection is likely to be restricted or denied. The coverage may state “no protection applies if the harm is attributable to a tree on a property the place the proprietor failed to keep up the tree correctly.” That is very true if the tree’s situation was evident to the property proprietor and so they did not take preventative measures.

Particular Conditions with Unlikely Protection

Sure conditions make protection for tree harm considerably much less seemingly.

- Timber on Personal Property: If the tree that fell was on non-public property, and never a public tree, the coverage may exclude protection. It’s because the policyholder might need some duty for timber on their very own property or the property of others.

- Timber on Public Property: Insurance policies typically exclude protection for harm from timber on public property, except the municipality or accountable get together is deemed negligent. Public entities typically have their very own insurance coverage insurance policies to deal with such incidents.

- Harm from Icy Branches: Harm from falling ice, even from timber, may not be lined if the ice buildup was indirectly attributable to a extreme climate occasion, however as a substitute by a gradual accumulation. Insurance policies often specify circumstances for ice-related protection.

Examples of Coverage Language

Coverage language varies considerably. Understanding the exact wording is important. Listed here are some examples:

“Protection for harm attributable to falling timber is excluded except the tree’s situation was not recognized to be unsound or diseased previous to the occasion.”

“Harm ensuing from pure disasters is roofed, however harm attributable to a tree’s failure as a consequence of pre-existing circumstances is excluded.”

“If the harm was attributable to a tree on property that the policyholder doesn’t personal, protection could also be restricted or denied, relying on the negligence of the property proprietor.”

Diminished Payouts

Insurance coverage corporations could argue for decreased payouts in the event that they imagine the policyholder contributed to the harm. For example, if the policyholder parked their automotive beneath a visibly unstable tree, they is likely to be held partially accountable.

Pre-existing Tree Situations and Negligence

Pre-existing circumstances of the tree and the negligence of the property proprietor are key elements. If the tree was visibly unhealthy, or the proprietor knew of its unstable situation and did not handle it, protection is likely to be restricted or denied.

Frequent Exclusions and Limitations Desk

| Exclusion Class | Description | Instance Coverage Language |

|---|---|---|

| Acts of God | Harm from pure disasters, however not essentially from timber. | “Protection for harm from windstorms, hail, and floods is offered, however not harm from timber falling as a consequence of pre-existing circumstances.” |

| Pre-existing Tree Situations | Harm attributable to a tree recognized to be unsound. | “Harm from falling timber shouldn’t be lined if the tree was recognized to be unsound or diseased previous to the occasion.” |

| Negligence of Property Proprietor | Harm from a tree on one other property the place the proprietor was negligent. | “No protection applies if the harm is attributable to a tree on a property the place the proprietor failed to keep up the tree correctly.” |

Claims Course of and Documentation

Submitting a declare for tree harm to your automotive can appear daunting, however a well-documented course of can easy the best way. Understanding the steps and mandatory documentation is essential for a swift and profitable declare. Insurance coverage corporations want clear proof of the harm and circumstances to course of your declare pretty.Thorough documentation is vital to proving your case and getting a good settlement.

This contains detailed pictures, police experiences, and witness statements. A transparent report of the incident helps insurance coverage adjusters perceive the scenario and assess the validity of your declare.

Steps Concerned in Submitting a Declare

Correctly documenting the incident is essential for a easy declare course of. A well-documented declare will increase the possibilities of a profitable final result. The steps contain reporting the harm promptly, documenting proof, and cooperating with the insurance coverage adjuster.

- Report the harm promptly: Contact your insurance coverage firm as quickly as potential after the incident. That is important for initiating the declare course of. Your insurance coverage coverage seemingly has a selected timeframe for reporting such incidents. Failure to adjust to this might have an effect on your declare’s validity.

- Doc the scene completely: Take detailed pictures of the harm to your car, the fallen tree, and any surrounding circumstances. Embrace close-ups of any seen harm, in addition to wider pictures of the whole scene. Notice the date, time, and climate circumstances. This gives essential proof for the declare.

- Acquire a police report: If potential, file a police report. This gives official documentation of the incident, together with the date, time, and any witnesses. A police report provides credibility to your declare and assists the insurance coverage adjuster in understanding the circumstances.

- Collect witness statements: If witnesses noticed the incident, gather their statements. A witness assertion gives beneficial details about the occasion, which might bolster your declare. Embrace the witness’s identify, contact info, and their account of the incident.

- Present detailed pictures of the harm: Excessive-quality pictures are important. Embrace photos of the whole car, exhibiting the extent of the harm. Shut-up pictures of scratches, dents, and different harm are essential for correct evaluation. Documenting the harm completely ensures a good settlement.

- Present copies of your insurance coverage coverage and documentation: This ensures the adjuster has the mandatory info to course of your declare. Evaluation your coverage to know your protection and any related exclusions or limitations.

Required Documentation

The next desk Artikels important paperwork and their significance within the claims course of. Having these paperwork prepared will velocity up the declare course of.

| Doc | Significance |

|---|---|

| Police Report | Supplies official documentation of the incident, together with time, date, and witnesses. |

| Witness Statements | Offers further particulars concerning the occasion, rising declare credibility. |

| Photographs of Harm | Visually paperwork the extent and nature of the harm to your car. |

| Insurance coverage Coverage | Supplies important particulars about your protection, together with coverage quantity and limits. |

| Automobile Registration | Confirms car possession and particulars. |

| Restore Estimates | Supplies a value estimate for repairs, supporting the declare quantity. |

Authorized Issues

Determining who’s accountable when a tree falls in your automotive includes extra than simply insurance coverage. Native legal guidelines and property proprietor obligations play a giant position in figuring out legal responsibility. Understanding these authorized facets can considerably influence your declare and the result of the scenario.Property house owners usually have an obligation to keep up their property in a manner that does not endanger others.

This contains protecting timber on their land wholesome and stopping them from falling and inflicting hurt. Nonetheless, the particular authorized necessities differ relying on the placement and the circumstances.

Property Proprietor Tasks

Property house owners have a authorized obligation to make sure their timber are correctly maintained. This contains common inspections, pruning, and removing of diseased or weak branches. Failing to meet this obligation might end in authorized repercussions if a tree falls and damages somebody’s property. Examples embrace conditions the place a home-owner uncared for to trim overgrown branches, leading to a tree limb falling on a parked automotive.

Legal responsibility for Damages

A property proprietor is likely to be held accountable for damages if their negligence contributed to the tree fall. This contains conditions the place a tree’s situation was clearly evident and the proprietor did not take motion. For instance, a home-owner is conscious of a big crack in a tree trunk however doesn’t take measures to have it assessed or repaired.

Tree Upkeep Legal guidelines and Protection

Native ordinances and rules typically dictate how timber needs to be maintained. These legal guidelines can considerably affect insurance coverage protection selections. If a property proprietor fails to adjust to native tree upkeep rules, their insurance coverage firm may deny protection, or cut back the quantity of compensation due.

Function of Legal responsibility Insurance coverage

Legal responsibility insurance coverage performs an important position in instances the place a tree falling from a property causes harm. If a property proprietor is discovered liable, their legal responsibility insurance coverage coverage will cowl the damages to the car. If the legal responsibility limits are inadequate, the proprietor could possibly be personally chargeable for the remaining prices.

Jurisdictional Variations

Authorized necessities for tree upkeep and legal responsibility differ considerably throughout completely different jurisdictions. Some areas have stricter rules relating to tree inspections and removing than others. For instance, states with increased wind speeds or extra frequent storms might need extra stringent rules on tree upkeep. Understanding the particular legal guidelines of your space is important.

Abstract Desk of Authorized Tasks

| Duty Space | Property Proprietor’s Obligation | Potential Outcomes |

|---|---|---|

| Tree Upkeep | Common inspections, pruning, and removing of hazardous timber. | Legal responsibility for damages if negligence is confirmed. Potential denial or discount of insurance coverage protection. |

| Legal responsibility Insurance coverage | Protection for damages attributable to tree fall, if legal responsibility is established. | Inadequate protection might result in private monetary duty. |

| Jurisdictional Variations | Variations in tree upkeep rules and authorized requirements throughout areas. | Variations in legal responsibility requirements and insurance coverage protection availability. |

Illustrative Case Research

Understanding how insurance coverage corporations deal with claims for timber falling on vehicles includes taking a look at real-world examples. These case research spotlight the complexities of proving negligence, establishing damages, and navigating jurisdictional variations in figuring out protection. Various factors, such because the situation of the tree, the climate patterns, and the placement of the incident, all play a big position within the final result of the declare.

Case Research Examples, Does insurance coverage cowl tree falling on automotive

A number of elements affect the result of a tree-fall declare. These embrace the tree’s well being, climate circumstances, and the claimant’s position within the incident. For example, if a tree is demonstrably diseased or in a state of decay, the insurance coverage firm could also be extra prone to settle for duty. Conversely, if the climate was terribly extreme, making the tree’s fall unavoidable, the insurance coverage firm may argue in opposition to protection.

Moreover, if the claimant was conscious of the precarious situation of the tree and took no motion, protection could possibly be denied.

Jurisdictional Variations

Completely different areas have various authorized requirements for tree-related property harm claims. Some jurisdictions might need stricter rules on tree upkeep, which might affect the result of claims. For example, if a home-owner is required to keep up their timber to a sure customary, and a falling tree damages a car, the insurance coverage firm may deny protection if the home-owner failed to satisfy this customary.

Conversely, if the tree fell as a consequence of an unprecedented climate occasion, the court docket could rule in favor of the claimant, no matter native tree upkeep rules.

Efficiently Obtained Protection: A Case Research

A house owner, Ms. Emily Carter, skilled a tree fall throughout a extreme storm. The tree, positioned in a wooded space behind her property, was deemed to be in a state of superior decay by an arborist. The storm’s depth, whereas extreme, was not unprecedented within the area. Ms.

Carter had no prior data of the tree’s situation. The insurance coverage firm initially denied protection, citing the home-owner’s duty for sustaining timber on her property. Nonetheless, the arborist’s report and meteorological knowledge demonstrating the storm’s depth offered robust proof supporting the declare. The insurance coverage firm finally agreed to cowl the damages, recognizing the tree’s decay as a big issue within the incident.

Abstract Desk of Case Research

| Case Research | Tree Situation | Climate Situations | Declare Final result | Jurisdiction |

|---|---|---|---|---|

| Case 1 (Ms. Carter) | Superior Decay | Extreme, however not unprecedented storm | Protection Granted | State X |

| Case 2 | Wholesome, however excessive winds | Unprecedented excessive winds | Protection Granted | State Y |

| Case 3 | Useless however not visibly harmful | Regular winds | Protection Denied | State Z |

Closure

So, does insurance coverage cowl a tree falling in your automotive? It is a complicated query with no simple reply. It is dependent upon a mess of things, out of your particular coverage to the circumstances surrounding the incident. Hopefully, this overview has offered a clearer image of what to anticipate when submitting a declare for tree-related automotive harm. Now, go forth and drive safely, and should your timber keep grounded!

Detailed FAQs

Will my complete insurance coverage cowl a tree falling on my automotive?

Complete protection typically covers harm from issues exterior of your management, like falling timber. Nonetheless, particular exclusions may apply, so test your coverage rigorously.

What if the tree was already weak or diseased?

A pre-existing situation of the tree may have an effect on protection. The insurance coverage firm may argue that the harm was foreseeable, probably impacting the declare. It is a difficult scenario.

Does the placement of the incident matter?

A rural location may improve the chance of tree-related harm in comparison with an city setting. This might have an effect on the insurance coverage firm’s analysis of the declare.

What if the property proprietor was negligent?

If the property proprietor was negligent in sustaining the tree, it might have an effect on the declare. The main points of negligence can be key right here.